Loading...

Articles

Analysis and assessments on DFS

Infographics

Visuals produced by DFS

⏳

Go back in time

Explore our Insights archive and discover past publications.

Explore our Insights archive and discover past publications.

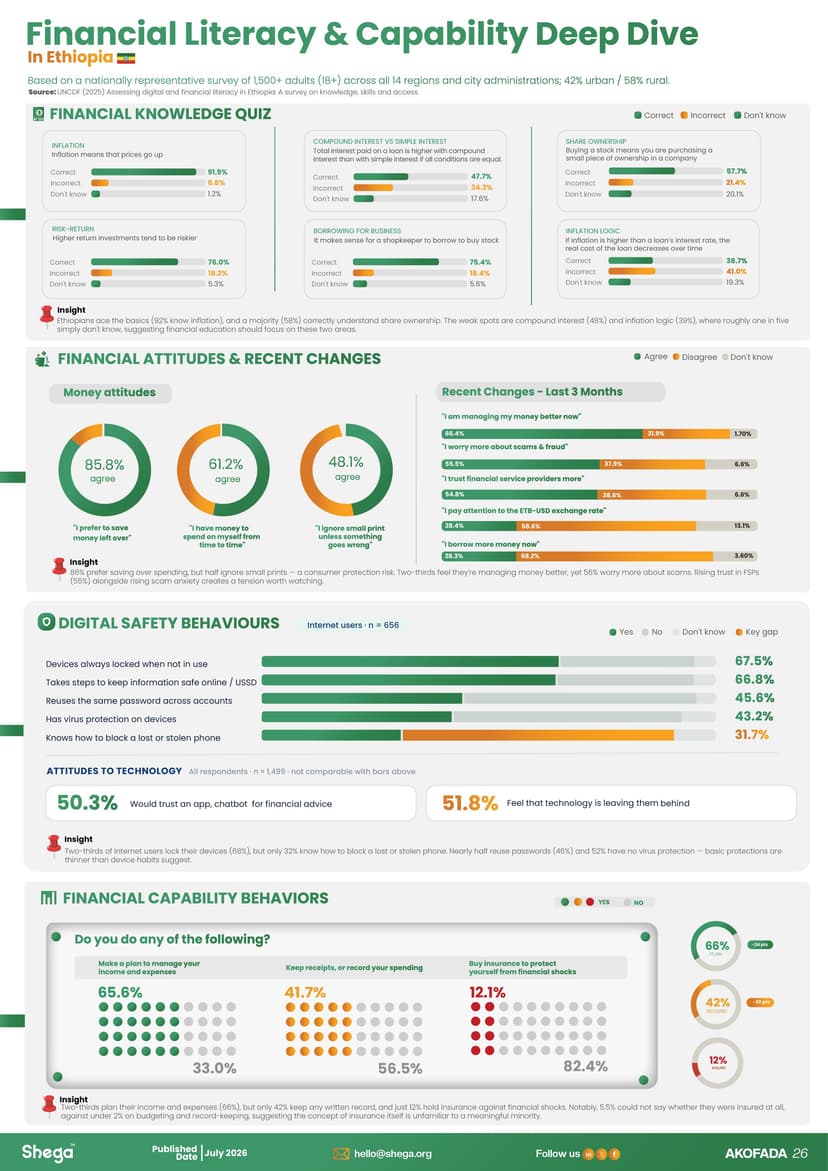

This infographic, "Financial Literacy & Capability Deep Dive in Ethiopia," was developed by Shega under the AKOFADA proj...

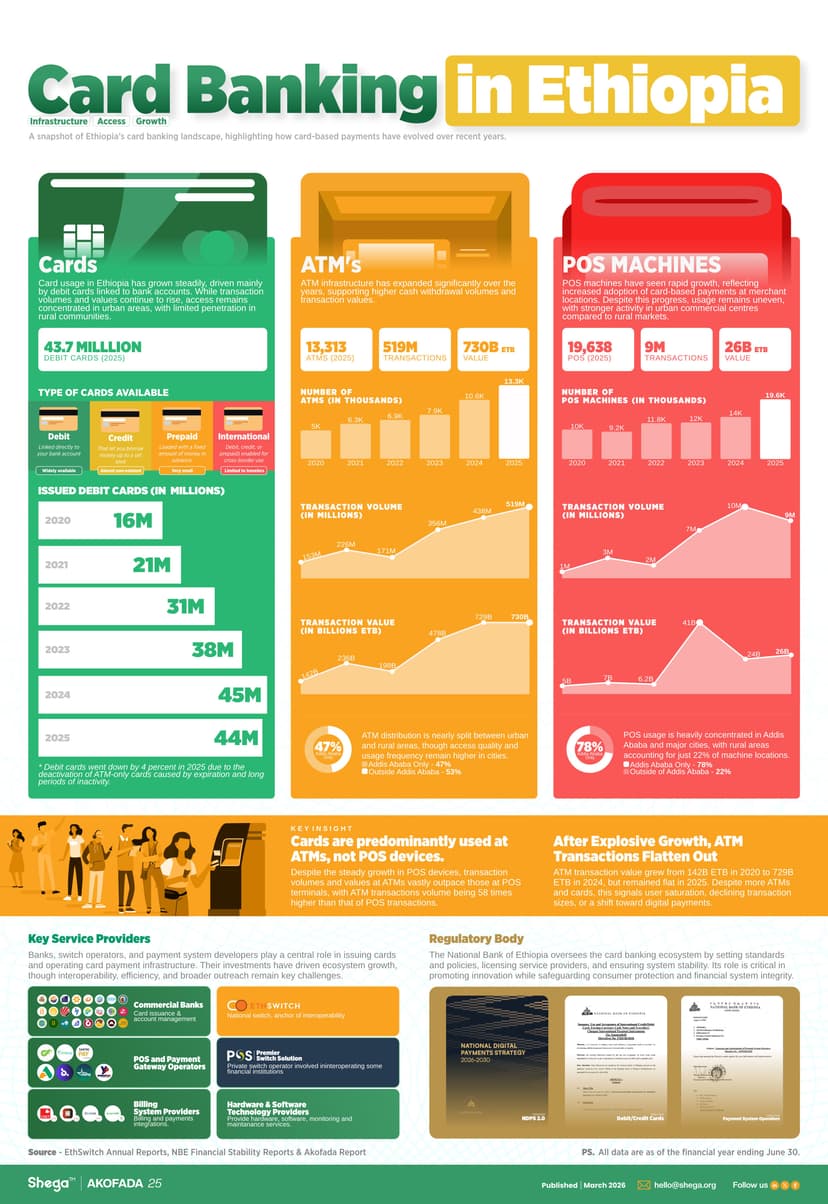

This infographic explores the evolution of Ethiopia’s card banking ecosystem, highlighting rapid infrastructure expansio...

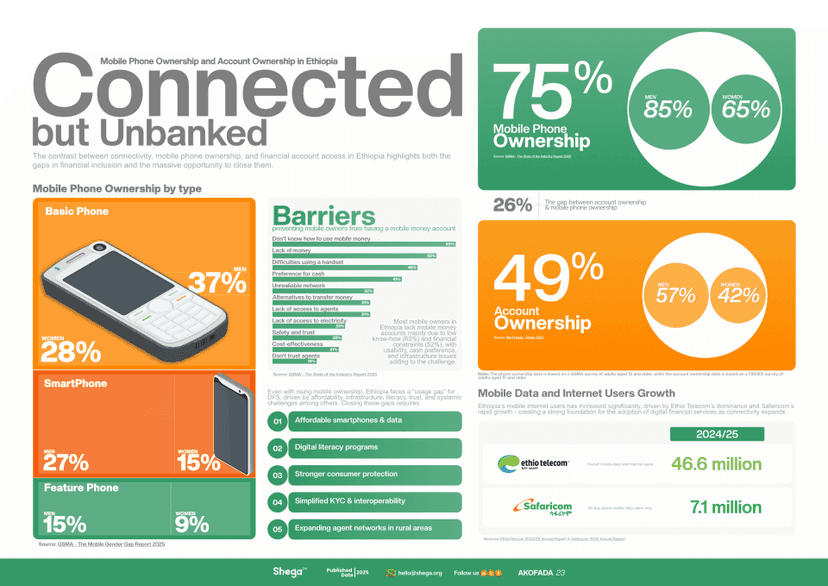

Ethiopia’s mobile money ecosystem is expanding, but adoption remains uneven. While most adults now own mobile phones and...

Ethiopia is experiencing one of the fastest digital connectivity surges in Africa — mobile internet users grew significa...